After enjoying a strong market rebound following the ‘Covid-crash’ of March 2020, late 2021 and the start of 2022 have been much more challenging for investors. Accompanying the adjustment to the idea of longer-term inflationary pressure, we have seen a sharp style rotation from the growth-oriented pandemic winners into the unloved sectors of the market traditionally benefitting from a rising rate environment. Throw in an escalation in geopolitical tension and the very real possibility of conflict on European soil, and one would be forgiven for feeling a little jittery.

In environments such as these, it is tempting to bend our investment philosophy in an effort to attempt to take advantage of short-term market movements. Unfortunately, by the time the direction of the shift becomes clear, it is often too late to join the party, meaning we chase trends which are already nearing their maturity. It is painful to miss out on relative outperformance, but we believe it would be even more painful to be burned by following the crowd and deviating from our long-term principles.

We will therefore remain resolutely committed to our pursuit of long-term outperformance through thorough fundamental research. In considering the main factors influencing markets today, it is challenging not only to identify the likely direction of travel, but also to identify the likely market response to different outcomes. In this piece, we will dive into historical ‘conflict’ events in an effort to frame possible market responses should the ‘worst-case’ scenario unfold. We will also consider the theoretical underpinnings of the current inflationary predicament faced by policymakers in an effort to better understand the potential medium to long-term outcomes.

Historical conflicts as a guide for geopolitical tensions

A significant uncertainty facing markets currently is the heightened geopolitical tension engulfing Russia and Ukraine, with concerns that conflict may escalate. Whilst the economic consequence of this would be severe, the human cost would clearly be catastrophic. We cannot begin to understand or articulate the implications of this type of development, and the importance of implications for investment portfolios pale in comparison to the real world consequences for our European and Russian neighbours. That said, we recognise that periods of instability and potential conflict can cause clients significant concern, particularly when it is close to home. We therefore provide a brief analysis below in an effort to present some historical scope to possible market reactions.

We found that during heightened levels of geopolitical risk (e.g. during the Gulf War or Annexation of Crimea), safe-haven assets such as Gold and 10-year US Treasury bills do offer some downside protection. However, maintaining a long-term view and riding out the volatility associated with such events, by remaining invested in risk-on assets, has tended to outperform.

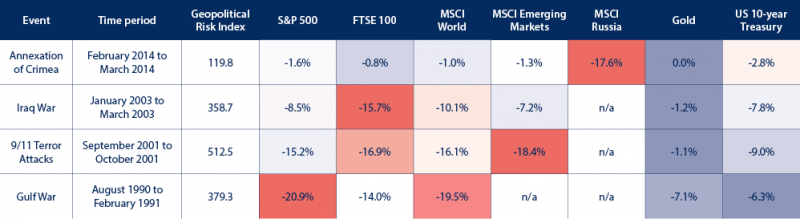

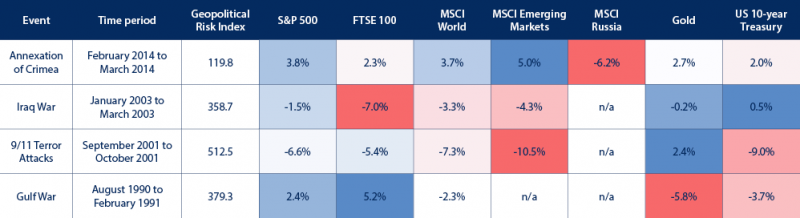

To assess the potential market impact of an escalation in tension between Russia and Ukraine, we have considered previous geopolitical events. The analysis below focuses on the Annexation of Crimea in 2014, the Iraq War in 2003, the 9/11 terror attacks in 2001 and the first Gulf War in 1990. To assess the risk of these events, we have used the Caldera and Iacoviello Geopolitical Risk Index (GPR). This index measures adverse geopolitical events based on a tally of newspaper articles covering such tensions. To provide context to the risk scores below, on 1 January 2022 the GPR stood at 108.97, which is slightly below the level reached in 2014 during the Annexation of Crimea.

Table 1.1 – Maximum downside of Index/Asset since start of period

Source: FE Analytics

Table 1.2 – Cumulative Return of Index/Asset during period

Source: FE Analytics

Table 1.1 summarises the maximum downside of the various indices/assets during each geopolitical event. Interestingly, the Annexation of Crimea in 2014 did not have any material impact on global markets, with negative sentiment limited to Russian investments.

During globally significant geopolitical events there tends to be widespread contagion in equity markets, with little protection offered by risk-on assets in terms of downside. However, Table 1.2 shows that remaining invested in risk-on assets will typically allow recovery of value from the maximum downside prior to the event risk subsiding.

This simple analysis provides three key insights:

- Avoid significant exposure to countries which can be deemed highly susceptible to geopolitical risk

- During globally significant geopolitical events, have exposure to risk-off assets to offer downside protection, particularly in lower-risk portfolios

- Maintain a long-term investment horizon and remain invested to ride out volatility associated with geopolitical events

Although in overall market terms, an escalation in tensions is unlikely to have severe, prolonged effects, short-term volatility could be uncomfortable. In addition, the economic response is likely to be felt more widely than the directly impacted regions. The industry most likely to be affected is Oil and Gas, where Russia remains a key supplier. With energy prices already rising dramatically in 2021, further pressure on supply would be a contributor to more persistent inflation, as discussed below.

The nature and scale of any military conflict is hard to predict. However, historical analysis suggests that we can be somewhat reassured, in investment terms, by falling back on our preferred approach: remaining invested in a long-term focussed, diversified multi-asset portfolio.

Inflation – where do we go from here?

In our Outlook for Investment for July 2021, we wrote:

We believe that inflation is likely to continue to rise from current levels and that the pressure may prove more enduring than the current rhetoric from central banks suggests. We also believe that policymakers are likely to accept systemically higher levels of inflation in the medium term in an effort to erode debt levels in a politically palatable manner. Although neither of these views predicates a steep rise in interest rates, we expect renewed volatility in equity and bond markets as investors struggle with an evolving economic environment.

Heightened volatility in response to persistent inflation and the start of less accommodative monetary policy does not come as a shock to us. In this section, we dive deeper into the drivers of inflation and the challenges faced by policymakers in responding to them.

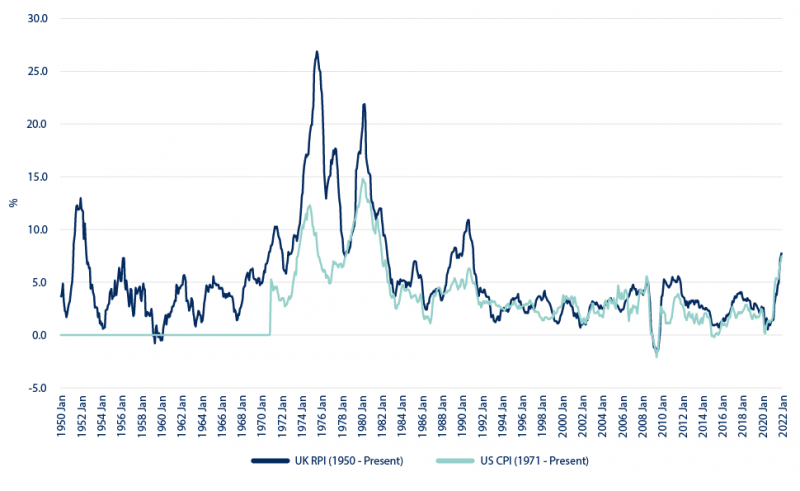

The UK, like many developed economies around the world, has enjoyed an extremely benign inflationary environment since the early 1990s. In recent months, external factors – notably energy and tradeable goods prices – have added inflationary pressure in regions which are net importers of these commodities. Central Banks have started to shift their tone away from the suggestion that this is purely a ‘transitory’ shock, towards an acknowledgement that higher prices may persist over longer term horizons. Whilst the Bank of England and Federal Reserve both maintain that inflation will fall back towards ‘target’ levels over two to three years, the interim period of rising prices provides a politically palatable way to ease the additional debt burden taken on during the pandemic.

Historical Inflation

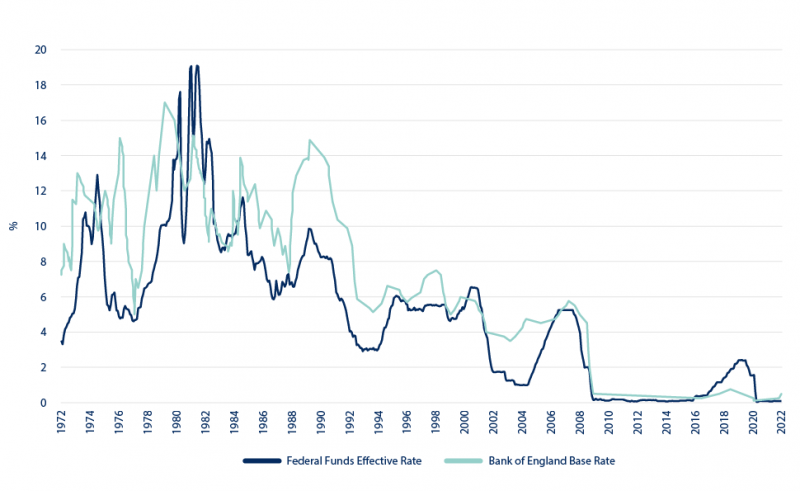

The recent decades of low inflation have been enjoyed alongside a remarkable environment for monetary policy. The Bank of England base rate has sat below 1% since the Global Financial Crisis, but even in the years before that shock, interest rates had fallen from a high of nearly 15% in 1990 to around 5% in 2008. The traditional economic wisdom surrounding the roles of fiscal and monetary policy in driving growth whilst curtailing inflation has not been as applicable to our most recent cycle as it has in the past.

US vs UK Interest Rate History

The current spike in inflation has been primarily driven by supply side factors. It is easy to buy the argument that production will take time to ramp up again following a global economic shutdown of the like experienced in 2020-21. In most cases, capacity is not like a tap which can be turned on and off – decommissioning and recommissioning systems comes with a lag.

In the energy markets, there are a number of other factors at play: political incentives to alter supply; weather; and an increasing drive towards investment in renewable alternatives can all have dramatic effects on market dynamics. Within the UK, there have also been transitory costs associated with the departure from the European Union and related increase in the cost of trade. None of these factors can be tackled effectively by Central Banks.

In other words, the current inflationary pressure faced in developed markets is what is known as ‘cost-push’ inflation. Rising raw material costs have fed through to consumers both directly in their demand for energy, and indirectly through companies raising prices to offset higher input costs.

Typically, market forces would take care of supply constraints: as prices rise, the reward for companies producing items facing shortages increases so more producers enter the market, thus increasing supply. This dynamic is what has led Central Banks to class the most recent inflationary surge as ‘transitory’.

The challenge for policymakers comes when cost-push and ‘demand-pull’ inflation combine in a fragile economic environment. Demand-pull inflation describes an environment in which an increase in demand from governments and/or households ‘bids up’ prices for goods and services.

We can see examples of this emerging in demand across several sectors of the economy. Increasing demand for semiconductors, for example, has led to rising car prices and product shortages, ranging from dishwashers to smartphones.

To exacerbate the issue, labour market dynamics in both the US and UK are presenting challenges. Unemployment rates have fallen consistently in recent decades and labour markets are now very tight. In a tight labour market, workers can demand higher wages. With the cost of living rising, both new and existing employees are further inclined to demand pay rises. Pay rises tend to be sticky – if wages and salaries increase in response to a short-term shock, they are unlikely to fall once the supply side pressures have eased and prices begin to fall. This leaves households relatively much better off and leads to higher levels of consumption, further increasing inflationary pressure.

A combination of these factors is making the environment difficult for those tasked with tackling inflation.

Investment Implications

Walking the line between supporting an economy recovering from a truly unprecedented shock and ensuring we do not enter an inflationary spiral is a daunting task. Meanwhile, the implications for investment portfolios are profound. With inflation north of 5%, the ultimate ‘safe haven’ investment of cash has a significant cost associated with it. As the path of interest rates becomes increasingly clear, a bear market for bonds has begun in earnest. At the same time, we have seen in recent months how volatile equity markets can be in the face of tapering, particularly those sectors trading at the dearer end of the spectrum.

So, where does one go? We revert to our long-term principles. We have no way of knowing how transitory, or otherwise, this latest bout of inflation will prove to be. Similarly, we do not know how policymakers will respond, or how markets will respond to policymakers. What we do know is what kind of company is likely to withstand a difficult economic environment like that discussed above. High quality companies with the ability to increase prices to preserve margin, operating in industries offering attractive prospects for growth, and trading at ‘reasonable’ valuations. Combine this with an asset allocation overlay providing exposure to regions facing different pressures, and we hope to diversify away some of the country-specific risk associated with our investments.

Outside of the equity bucket, we again look to diversity of asset class to help us through an uncertain economic environment. In fixed income, we look to reduce the sensitivity of bond holdings to interest rate changes, whilst searching for modest yields to offset the impact of inflation. Property and infrastructure buckets provide real asset exposure and a high degree of inflation linking in the underlying cashflows. We also believe that the current environment warrants renewed discussion on the merits of alternative assets such as absolute return, macro strategies and commodity funds, but recognise that these options also present challenges.

It is easy to get drawn into a negative news cycle when confronted with challenges. It is worth remembering that many difficult situations have positive consequences. One of the factors driving rising cost pressure is increased corporate and government spending on technology – this is likely to be positive for productivity in the long-term. Cost pressure has also often historically driven innovation. Rising energy costs are, in part, a result of reduced investment in fossil fuel generation in favour of more climate friendly alternatives; whilst painful in the short run, the potential long-term benefits are clear.

Conclusion

Our conclusion to this Outlook remains remarkably consistent with those that preceded it. Whilst several of the themes that we have discussed previously have played out as we anticipated, our portfolios have been on the wrong side of a sharp market rotation over the last year. We strongly believe that continued discipline in selecting strategies with attractive long-term prospects will provide clients with the best possibility of sustainable returns across different economic environments.

As always, our Investment Committee endeavours to be responsible in all investment decisions and seeks only to select investments which are in the best interests of clients. We are committed to the highest standards of research and insist on the same standards where external fund managers are recommended. The processes, policies and procedures of fund managers form a central part of our analysis of external managers and we will continue to assess potential investments across a wide range of quantitative and qualitative criteria.

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.