What is the US Debt Ceiling?

The US debt ceiling is a limit, imposed by Congress, on the amount of money that the US government is allowed to borrow. The US government operates on a budget deficit, i.e. it spends more on services such as social security, healthcare and the military than it collects in taxes and other revenue, hence the need for the US government to borrow. The US treasury typically issues government bonds to raise money, but they can only do this up to the debt ceiling, at which point, they cannot borrow further. The US hit the current debt ceiling (c.$31 trillion) in January 2023 and has been using special accounting measures ever since – a temporary fix that can buy them several extra months. It is currently estimated by the Treasury that they will exhaust these measures and be unable to pay the government’s bills as early as 1 June.

This limit has been a contentious political issue in recent years, as the government has come up against the debt ceiling several times, leading to threats of government shutdowns and defaults on US debt. For context, the debt ceiling has been raised seventy-eight times in the last sixty-three years, it has been raised more than one hundred times since its inception in 1917 and it has been raised under every single president since Hoover (1929-1933). Congress has also suspended the debt limit seven times since 2013 so it’s not a particularly novel situation.

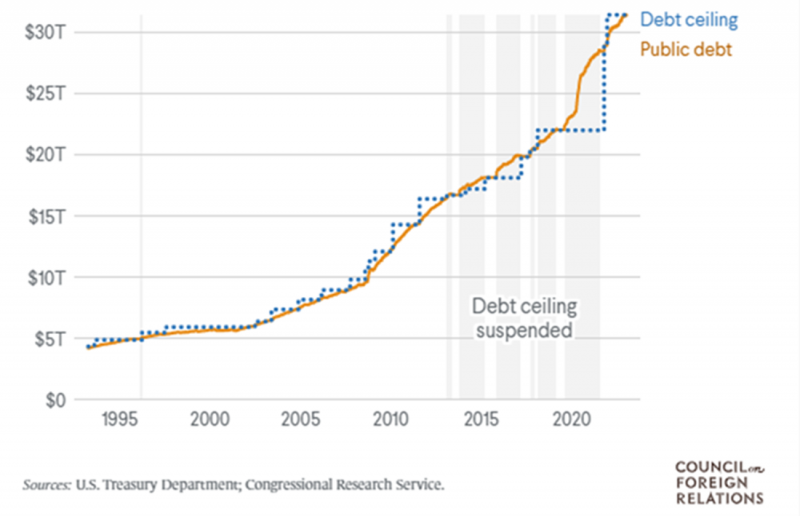

U.S. Debt has sometimes risen faster than the Debt Ceiling

(Berman, 2023)

Why haven’t Congress raised the debt ceiling already?

Congress can simply vote to raise the debt ceiling again, however, the House of Representatives has a Republican majority and they are leveraging the debt ceiling deadline to get Biden to agree to spending cuts. On 26 April, a debt ceiling bill was passed in the House to raise the limit by $1.5 trillion under the condition that government spending would be cut by $4.8 trillion over the next ten years. It is highly unlikely that the bill will pass through the Senate and be approved by Democrats, hence the stalemate. Democrats are adamant that spending cuts should be budget negotiations and not tied to the debt ceiling whilst the US hurtles towards a default.

This is not the first time we’ve seen Politicians hold the debt ceiling hostage and unfortunately it has been a successful strategy in the past. 2011 is perhaps the most infamous example whereby Democrats eventually caved and agreed to spending cuts just three days before the government defaulted. This debate led to government shutdowns and just the threat of a default resulted in a downgrade of the US’s credit rating by Standard & Poor’s and heightened market volatility.

What happens if the US default on their debt?

If the US were to exceed the debt ceiling, it would be unable to borrow any more money to pay for its obligations, including public sector salaries and servicing its debt. This would force the government to either default on some of those obligations or make significant cuts to its spending. Defaulting on its debt, widely considered one of the safest assets in the financial system, would undoubtedly have devastating economic consequences. Likely, it would damage the US’s credit rating, increase borrowing costs (not just in the US but all around the globe), weaken the US dollar, trigger a spike in unemployment and throw the value of its government debt into turmoil. The US dollar’s status as the world’s reserve currency would be called into question.

The majority (69%) of US debt is held within America, with the rest (31%) being foreign-owned. Japan is the largest holder of US Treasury securities, with around $1.1 trillion. China and the UK hold $867bn and $654bn respectively. 60% of the world’s foreign currency reserves are also held in dollars so the implications of a default are global. US treasury secretary, Janet Yellen, said “Failure to meet the government’s obligation would cause irreparable harm to the US economy, the livelihoods of all Americans and global financial stability.”

Whilst it is estimated that a default would immediately halt 10% of US economic activity in the worst case, tipping the economy into a recession, it’s not the end of the world; everything wouldn’t just stop. The US government can still spend all its other income e.g. from taxes, the Treasury Department would just have to prioritise who gets paid first and effectively function at a reduced capacity. Undoubtedly, the holders of government bonds would be a top priority to avoid defaulting on US debt and to minimise the damage to the creditworthiness of US Treasuries and thus the US dollar. This would likely come at the unfortunate expense of government salaries, retirement benefits and national defence spending.

What is likely to happen this time?

In the face of causing a global financial crisis, one has to hope that the US government will reach a deal, just like in 2011 (and numerous other times). In fact, Goldman Sachs’ base case is a resolution on deadline day, plus or minus one day. There is no doubt that the US can afford to pay its debt and a default would be entirely man-made. The most likely scenario is that Biden and McCarthy will negotiate and reach a compromise, although it’s not out of the realm of possibility that the Democrats will get their clean debt ceiling bill. The other option is to push it further down the road, either by temporarily suspending the debt limit or by agreeing to a small increase just to buy more time for negotiations and sync the debt limit deadline up with a budget negotiation.

Unfortunately, part of the damage is already done. 2011’s credit downgrade reflected weakened confidence in the US’s ability to manage its debt which has been shown once again. Even without a default, another downgrade is possible and this would cause much of the same repercussions previously mentioned for a default e.g. increased borrowing costs (for the government, businesses and consumers) and a weaker US dollar. Also this is not 2011, government debt back then was at 65.8% of GDP, now it’s at 98% and interest rates are much higher – the cost of servicing its debt is significantly greater, even more reason to reach a deal.

What about liquidity?

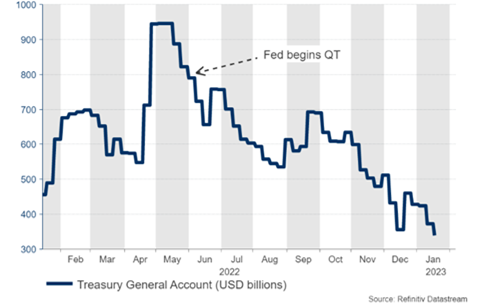

In conjunction with the ‘extraordinary measures’ that the Treasury are using, they are also depleting the Treasury General Account (TGA) to pay its obligations. This is injecting liquidity into markets in a comparable way to Quantitative Easing. So, whilst the Fed have been on their tightening cycle, the Treasury have been pumping enough money into the markets to more than offset the Fed’s liquidity reductions this year, i.e. increase liquidity on a net basis. This liquidity has helped drive asset prices higher in the US.

Treasury depletes cash buffer at the Fed

Treasury essentially injecting liquidity back into markets

(Hadjikyriacos, 2023)

The party can’t carry on though and eventually, when a deal is reached on the debt ceiling, the Treasury will begin to rebuild the reserves in the TGA. This would remove liquidity from the market at a time where the Fed is also tightening resulting in ‘liquidity removal on steroids’. A debt ceiling bill, therefore, might bring a wave of relief to bond markets, but the implications to equities, at least over the mid-term, may not be as positive.

References

Berman, N. (2023, May 02). What happens when the US hits its debt ceiling? Retrieved from Council on foreign relations: https://www.cfr.org/backgrounder/what-happens-when-us-hits-its-debt-ceiling

Hadjikyriacos, M. (2023, January 25). US debt ceiling matters this time, here’s why. Retrieved from XM: https://www.xm.com/research/analysis/specialReports/xm/us-debt-ceiling-matters-this-time-heres-why-special-report-173448

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.