1 January 2023

Introduction

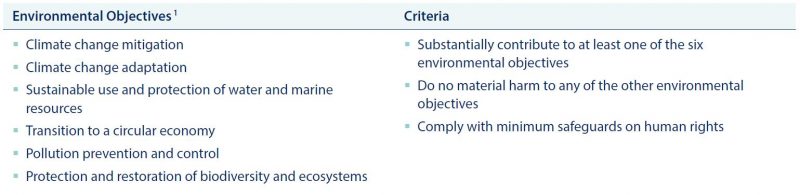

The UK Green Taxonomy is a science-based classification system aimed at accelerating green finance initiatives, by addressing the problem of Greenwashing and thereby supporting the UK’s transition to a net-zero economy. The foundation of the Taxonomy is based on the EU Taxonomy, which outlines that for an activity to be ‘Sustainable’ or ‘Taxonomy-aligned’ it needs to follow at least one of six environmental objectives and meet three criteria, which are illustrated below:

The taxonomy will build on existing international taxonomies and will serve as a common framework to set the standard for investments defined as environmentally sustainable in the UK.

Implementation

The Green Technical Advisory Group (GTAG), comprised of key financial market stakeholders and subject matter experts, will review the appropriateness of the metrics for the UK, develop a technical screening criterion (TSC) to underline each of the six environmental objectives and provide independent and non-binding advice to the government for implementing the taxonomy in the UK.2 The TSC for climate change mitigation and climate change adaption are the first two objectives on the agenda to be discussed and reviewed. This format follows a similar approach to the implementation of the EU Taxonomy, which released the TSC for the first two objectives in advance of the other four objectives.3

The Taxonomy will accept “Transitional Activities” and “Enabling Activities”. Transitional Activities are those in which technological constraints do not currently permit achieving full decarbonisation but are essential for transition whilst other solutions are not yet available. Hybrid cars, before the technological advancements in electric vehicle manufacturing, are one example. In this regard, Transitional Activities will be accompanied by timelines anticipating when new technology will have overtaken these activities and they can no longer be labelled as green or sustainable.4 Enabling Activities are those that enable other activities to contribute to decarbonisation or environmental objectives, even if they are not sustainable themselves (e.g., wind turbine components).

The Taxonomy will be drawn up alongside the UK Sustainability Disclosure Requirements (SDR). Assessment and disclosure against UK Green Taxonomy will also form part of the input for the SDR to ensure consistency and will be designed to ensure reporting requirements are in line with the recommendations of the Task Force on Climate-related Financial Disclosures (TCFD). This will be rolled out across the UK economy by 2025. The disclosures will be consumer-facing. This means that investment product providers will have to publish consumer-facing disclosures relating to the impact, risk and opportunities associated with their products. No exact timescale has been placed on the requirements yet.5

Investment Implications

Potential investment implications, resulting from the Taxonomy implementation, are listed below:

- Greater disclosure and transparency requirements are likely to lend structural support to data providers and financial technology companies

- Companies producing enabling products or technologies are also likely benefactors

- Green Finance initiatives might become mainstream sooner and prove attractive for inclusion in investment portfolios

- The integration of governance and social aspects in the estimation of a company’s cost of capital and risk and return profile is likely to reformulate the perception of certain sectors and industry valuations

1 EU Technical Expert Group on Sustainable Finance (2020), “Taxonomy: Final report of the Technical Expert Group on Sustainable Finance”

2 Green Finance Institute, “UK Taxonomy – GTAG”

3 Latham & Watkins (2021), “UK Government releases roadmap to sustainable investing”

4 ESG Clarity (2021), “Here’s what the UK taxonomy should look like”

5 Financial Conduct Authority (2021), Discussion Paper, “Sustainability Disclosure Requirements (SDR) and investment labels

Risk Warnings. This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice as at 1 January 2023, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.