So far, 2020 has provided huge challenges. What began as a health emergency quickly developed into a potential social, economic and political crisis. Markets reacted hard and fast, with equities demonstrating volatility exceeding that experienced during the Global Financial Crisis.

Corporate bond markets showed concerning levels of liquidity, whilst ‘Alternative’ assets such as Property and Infrastructure provided little downside protection. Short duration Gilts, Cash and Gold were amongst the few asset classes spared from significant falls.

For the markets, recovery has come almost as fast as the drawdown. Improving health data and optimism around the reopening of economies, combined with massive fiscal and monetary packages, precipitated a ‘V-shaped’ bounce which few were anticipating. Significant uncertainties remain however, both in epidemiological and economic terms. The possibility of second waves of infection as economies reopen; an adjustment to a ‘new normal’ as vaccines and treatments are researched; a likely rise in unemployment as fiscal support schemes become unsustainable; and the ultimate burden of who will end up paying for the stimulus employed by governments and central banks are just some of the questions which face investors.

This outlook will focus on two areas where we see significant risk and opportunity for client portfolios over a long-term horizon: Inflation and the growth of Environmental, Social and Governance (‘ESG’) investing.

1. Inflation

Central Banks have universally signalled their willingness to ‘do whatever it takes’ to support economies in the face of this shock. The Federal Reserve lowered rates by 150bps to 0-0.25% in March. They took additional actions to provide up to $2.3tn in loans to support the flow of credit to households and businesses. This came in the form of new bond and loan issuance and a commitment to provide liquidity for outstanding corporate bonds. In Europe, although the ECB had limited capacity for rate cuts, they have introduced and strengthened existing purchasing programmes such as the Pandemic Emergency Purchase Programme (‘PEPP’) and the Asset Purchase Programme (‘APP’). Launched in March, the PEPP increased asset purchases of private and public securities by €1.35tn until at least June 2021 while the ECB increased their APP by additional net asset purchases of €120 billion until the end of the year.

The UK’s monetary policy initiatives came in the form of llower interest rates, development of lending facilities and the purchasing of gilts and corporate bonds. In March, the Monetary Policy Committee (‘MPC’) voted to reduce the Bank Rate from 0.50% to 0.10%. The Bank of England (‘BOE’) voted to increase their holding of UK gilts and sterling nonfinancial investment-grade corporate bonds from £445bn to £645bn. The BOE has also introduced facilities to provide assistance to large firms to bridge cashflow disruption and to allow banks and building societies to access four-year funding at close to Bank base rates to reinforce the onward transmission of the rate cut to businesses and households.

The fiscal response to the crisis has been equally impressive. In the US, a total of c.$3tn has been pledged across four major Acts. The largest of these, the Coronavirus Aid, Relief and Economy Security Act (‘CARES Act’) provides tax rebates for individuals and unemployment benefits amongst others, to the value of $2.3tn. A further c.$700bn has been directed at support for small businesses, hospitals and an expansion of virus testing. In Europe, the IMF estimates that national liquidity measures have amounted to €2.9tn. This includes support for health spending and businesses, as well as a relaxation of EU budgetary rules to allow expansive fiscal policy and a relaxation of EU state aid rules to allow support of critical sectors. In the UK, the Office for Budgetary Responsibility estimates the total cost of fiscal stimulus to be £132.5bn. A significant portion of this comes in the form of the government Furlough scheme, which has been extended until the end of October. Other areas of spending include additional support for the NHS, public services and charities, business support and increased Universal Credit payments.

Drivers of Inflation

There are a number of theoretical mechanisms by which inflationary pressure within an economy can increase. Cost-push inflation is driven by an increase in the cost of production – usually higher raw material or wage costs. Demand-pull inflation is driven by strong consumer demand for products or service, resulting in insufficient supply and higher prices. Often, demand-side and supply-side factors interact such that inflationary or deflationary pressure can come from both sources.

There is a commonly held view that expansionary monetary policy, particularly in the form of Quantitative Easing (‘QE’) will automatically lead to inflationary pressure. The mechanism for this is clear; QE involves a Central Bank purchasing bonds from commercial banks or other investors. The Central Bank will do so either using existing cash reserves, or by expanding the money supply (printing money). It follows that in either case, more cash will be in circulation in the economy, which under normal

circumstances, one would expect would lead to inflation.

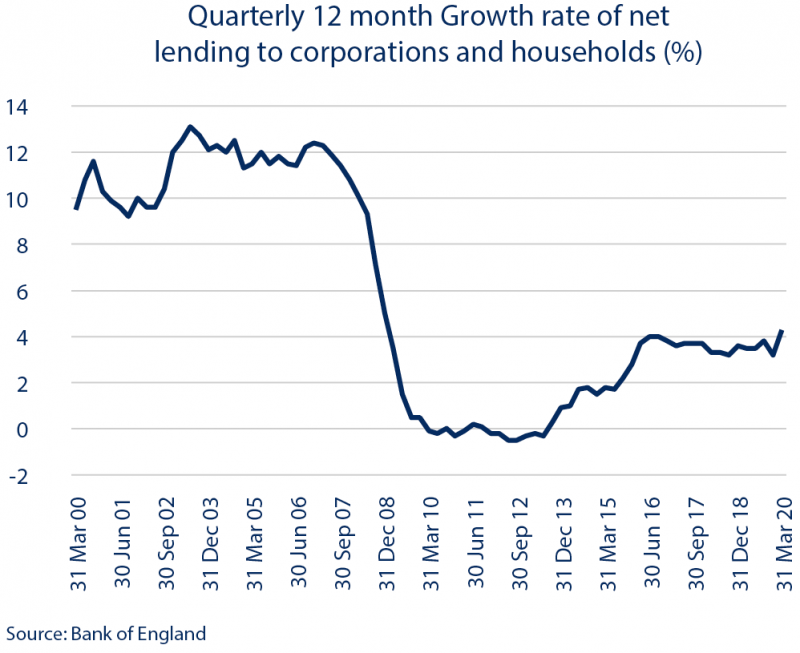

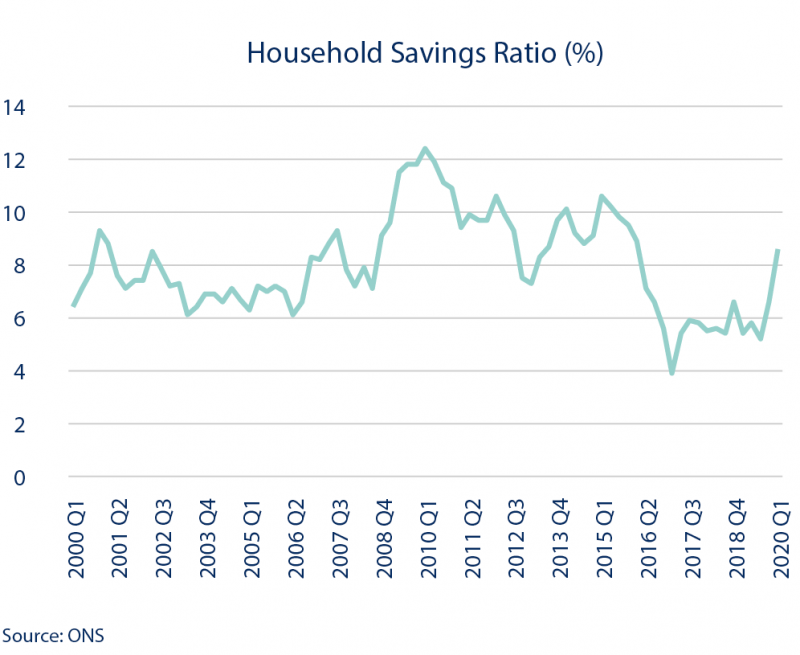

However, this conclusion rests on the assumption that commercial banks and/or investors will lend or spend the cash provided by the Central Bank. This may not always be the case, particularly in times of crisis, where banks would be inclined to reduce risky lending and consumers would be inclined to save rather than spend. This was evidenced during the GFC, with a significant drop in net lending by banks and a rise in the household savings ratio, despite significant QE and reductions in interest rates. We do not yet have data to monitor net lending since March 2020, but household saving has risen sharply in the UK in response to Covid-19 uncertainty.

Currently, we see a number of conflicting drivers for inflation in the UK and Global economy. An unprecedented fall in Global industrial demand due to lockdown measures shutting down economies, combined with geopolitical posturing amongst key oil-producing nations has led to significant downward pressure on oil prices. Deflationary pressure looks fairly significant on both the demand and supply side in the short-term.

Over the medium-long term, we would expect fiscal and monetary stimulus to counteract this short-term pressure. However, the extent of inflationary pressure will be determined by banks’ willingness to lend; consumers’ willingness to borrow and spend; and the extent at which businesses are able to return to ‘normal’ levels of economic activity. There remains significant economic uncertainty ahead, particularly around future unemployment once fiscal support is withdrawn. This is likely to hold back inflation, as savings rates increase both on corporate and consumer sides.

One of the features of this crisis is the monumental response of Central Banks and governments to support economies. This response has led to rapid increases in national debt, to levels not seen since World War II. Unlike the years following the Financial Crisis, there is currently no suggestion of austerity to reduce this debt burden, with a preference being shown for growth stimulus in an effort to increase the denominator rather than reduce the numerator in the Debt/GDP equation.

With Central Banks and governments holding record debt levels, an ‘easy’ option for reducing this over time is to allow higher inflation. Provided inflation is kept under control and there are no concerns around the legitimacy of the currency, policymakers are likely to view this as an attractive route forward. This is particularly true given the global nature of this crisis – most developed economies are in similar positions, making currency pressure less likely. As such, we believe that over medium-long term horizons, being holders of government debt will not be the most attractive place to be. One thing to learn from the market response to Covid-19 thus far is that it is favourable to be on the same side of the trade as the policymakers.

Investment Implications

With this in mind, we intend to continue positioning client portfolios to include real assets. For some time, we have been positive on real infrastructure assets and continue to recommend UK and Global options within this space. We are careful to differentiate between companies and structures with exposure to real assets such as toll roads, healthcare providers and renewable energy producers; and equity-based infrastructure which typically have high exposure to listed utilities and transport companies.

Another real asset which should theoretically benefit from rising inflation is Property. We find this sector more problematic given the unknown impact of changing working practices and economic uncertainty on the commercial real estate and retail sectors. We have recently reduced our Property exposure in our model portfolios, but remain open to opportunities in logistics, residential real estate and select commercial real estate, should they arise. There is often some crossover in holdings between Property funds and Infrastructure funds, particularly in the more attractive areas of healthcare and residential real estate assets.

Equities, generally, provide reasonable real returns in inflationary environments. Companies with pricing power are able to enjoy some degree of protection against inflation by passing rising costs on to consumers. We have historically favoured relatively strong equity weightings in our model portfolios, as we believe that over long-term horizons this will provide the best risk-adjusted returns for clients. However, given the current short-term economic uncertainty, our models have lower equity exposure than we would expect them to maintain over the course of a cycle. We will continue to monitor the market and economic environment, looking to add exposure where we see attractive opportunities.

Currently, we are overweight cash and short duration fixed income. Whilst we are comfortable with this positioning in the short-term due to limited inflationary pressure and significant uncertainty which is not fully reflected in stock markets, we are acutely aware of the long-term risks associated with this exposure. We maintain our view, expressed in past comments, that locking in negative returns by holding long-dated fixed income is not logical for long-term investors. The inclusion of index-linked bonds in portfolios could prove attractive in the event of higher inflation, but these assets have historically displayed equity-like levels of volatility. We anticipate continued changes to our fixed income positioning over time.

2. An acceleration of existing trends: ESG Investing

Global lockdowns, enforced in response to the spread of Covid-19, have served to accelerate a number of existing trends. A need to facilitate home-working has forced companies to invest in or improve infrastructure available to employees. A change in working practices on this scale provides a ‘natural’ experiment on a microeconomic and macroeconomic level into the productivity impact of workers being away from office environments. Similarly, in the world of education, virtual learning environments have advanced rapidly, with some higher education providers anticipating permanent changes in how courses are taught.

In retail, a state-mandated closure of physical stores has benefitted players with significant online presence. Obvious beneficiaries include large technology companies such as Amazon and Shopify, but also local winners such as Ocado. In the UK, online retailer Boohoo has continued buying the online businesses of troubled competitors. High street names Oasis and Warehouse recently joined Boohoo’s brand catalogue, following the acquisition of the online businesses of Karen Millen and Coast in 2019. We see further opportunities for investors, even in troubled industries, but believe there are likely to be additional casualties amongst the secular ‘losers’. This disparity is reflected in relative valuations; Boohoo now commands a market value exceeding 2.5 times that of beloved British favourite Marks and Spencer.

One investment trend which has been gaining traction in recent years is the rise of mandates focussing on Environmental, Social and Governance (‘ESG’) factors. We believe that this trend is likely to be accelerated by recent events; this presents both challenges and opportunities for our clients.

Challenges associated with ESG Investing

A primary challenge for investors in this space is one of definition. There remains a lack of consistency around the terminology used to describe ESG investing. The terms ‘ethical’, ‘sustainable’, ‘responsible’ and ‘ESG’ are often used interchangeably, without consensus over what each term should mean. The regulatory landscape for ESG corporate disclosure and ESG funds varies widely across jurisdictions, making it challenging for investors to apply consistent principles to global holdings.

As investor focus shifts further to ESG considerations, there are potentially very real challenges for businesses to overcome. Accurately measuring the carbon footprint of a global business, for example, requires significant data processing; the requirement becomes even more arduous if disclosure around the environmental impact of a product under an end user becomes necessary. Culturally, there are different expectations for the working practices in different geographies, making ‘Social’ policies for large institutions fraught with logistical issues. In Governance terms, companies are rightly focussing on gender equality and diversity at senior management levels, for example. Unfortunately, candidate pools are not always reflective of ‘optimal’ diversity targets; these are societal issues influenced by different educational opportunities, regional disparities within countries and deep-rooted differences in career choices between different demographics. It is hard to make an argument that companies should be solely responsible for addressing these types of issue; yet quantitative governance targets around Board representation for example, often expect them to do so.

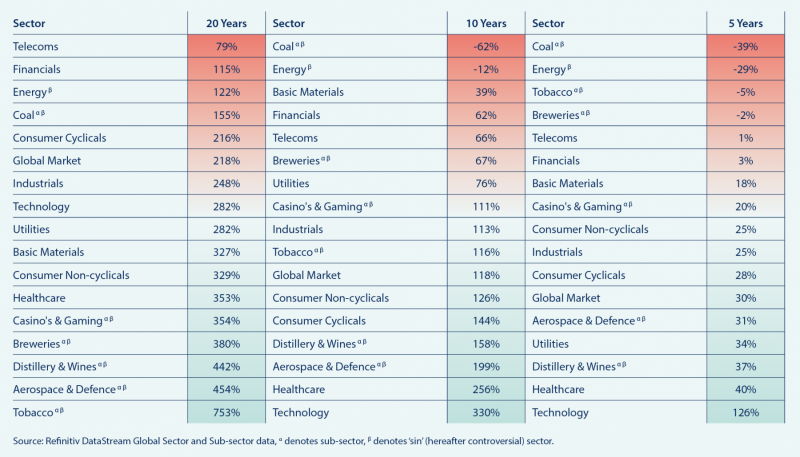

Many clients are concerned about the impact of incorporating ESG factors into their investment decisions on financial returns. This is a difficult topic to address, because the performance of ESG-mandated funds has historically been heavily influenced by the exclusion of traditional ‘sin’ sectors.

Examining the historic performance of controversial sectors demonstrates the issue. Over a 20-year horizon, the top five performing sectors would be excluded under many ESG mandates. Over 5- and 10-year horizons, Technology has been the standout sector; since ESG mandates do not typically exclude technology, an overweight here is likely to have been beneficial.

Potential Opportunity

Despite these challenges, we view the potential investment opportunity in ESG-mandated funds as attractive. Many of the principles behind selecting ‘ESG-friendly’ investments remain consistent with those that have been employed by prudent long-term investors for many decades. A focus on management and governance has always been important and remains so. Over the long-term, avoidance of declining industries is likely to be in clients’ best interests. There will remain questions over how to balance divestment and engagement, but these are likely to become easier as pressure mounts for ‘old’ energy providers to invest in future technologies. We do not subscribe to the principle that investing with ESG in mind necessitates a reduction in financial returns. Indeed, with prudent manager selection, we believe the opposite can be true. ESG-mandated funds have performed particularly well so far in 2020, with many avoiding Energy exposure which has been beneficial in the face of falling oil prices.

Application to Cantab portfolios

Within our main model portfolios, our focus continues to be the maximisation of financial return for clients. We require fund managers to provide their ESG policies, but ESG-specific mandates are not required. Our investment philosophy at Cantab has always included a desire to select managers with clear, understandable strategies; long-term horizons; and a focus on thorough fundamental research. Although we do not anticipate shifting the main models towards a ‘negative-screening’ approach, we do conduct thorough due diligence on our recommended managers and would expect them to be aware of, and engaging in, relevant ESG issues for their underlying holdings. Where we have concerns around a fund manager or house, we are fast and conservative in our actions for clients. Where we see opportunities in funds with ESG mandates, we will not hesitate to recommend these to the main models; indeed, we have recently added Baillie Gifford Positive Change for many clients within our Specialist Equity category.

For many clients, this approach provides the optimal balance between achieving their long-term investment goals and ensuring responsible stewardship of their assets. However, some clients wish to go further, by avoiding specific sectors or investing with a particular theme in mind. We have historically accommodated these special requirements by constructing bespoke portfolios on a client-by-client basis. However, with demand rising, we have recently launched some solutions which we believe will be attractive to clients going forward.

Firstly, the Cantab Global Sustainable Equity fund was launched at the end of last year, with institutions initially in mind. Our institutional clients and prospective clients have come under increasing pressure to engage with ESG principles, driving us to develop an equity fund with this in mind. Secondly, we have launched an ESG multi-manager portfolio. Developed with the same philosophy and principles as our main model portfolios, the ESG model includes only funds with specific ESG mandates. Whilst these mandates will not all approach the issue in the same way, we believe this is an attractive first step for clients who wish to exclude traditional ‘sin’ sectors from their investments whilst maintaining the balanced asset allocation and different risk profile options that accompany our model portfolios. Client directors would be delighted to discuss these, should they be of interest.

Investment Conclusions

1. Significant economic uncertainties remain; in the short-term, we are comfortable retaining a relatively defensive position for clients

Thus far, policymakers have successfully navigated a remarkable challenge. However, fiscal support is not indefinite and we believe that we will see further economic consequences of the lockdown. Until a vaccine is found, normality is unlikely to return and the possibility of further waves will impact corporate and household spending decisions. With equity markets currently looking fairly optimistic and inflation muted, we believe it prudent to retain some dry powder in portfolios until we have greater clarity on future economic conditions.

2. In the medium-long term, inflationary pressure is likely – portfolios should be positioned accordingly

With sharp increases in global government debt levels, we believe there is an incentive to allow moderate levels of inflation in the medium to long term. The extent of inflationary pressure will depend on the economic consequences of lockdown, particularly on consumption and investment decisions. Our longstanding attraction to real assets should serve portfolios well and we intend to reduce exposure to short duration gilts and cash over the coming months.

3. Lockdown is accelerating a number of pre-existing trends, including the rise in popularity of ESG Investing

The relative outperformance of ESG-mandated funds during the market drawdown is likely to further increase their appeal to investors. We believe that this area of investment is still very much in its infancy, with many challenges for investors and companies to address. However, the regulatory environment is moving quickly in this area and advisors and institutions, in particular, will need to be confident in their approach. We see significant opportunities, both in terms of dedicated ESG-mandated portfolios and in the inclusion of outstanding ESG funds in standard portfolios.

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.