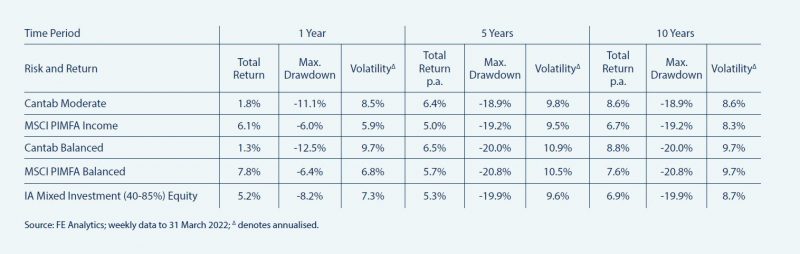

Risk and Return

The table below summarises the total return, maximum drawdown and volatility of the Cantab portfolios alongside their respective benchmarks:

Over the last ten years, the Cantab portfolios achieved material outperformance over their respective benchmarks and achieved these returns with relatively lower maximum drawdowns. Annualised volatility of the portfolios over the last decade are in-line with their respective benchmarks over most horizons.

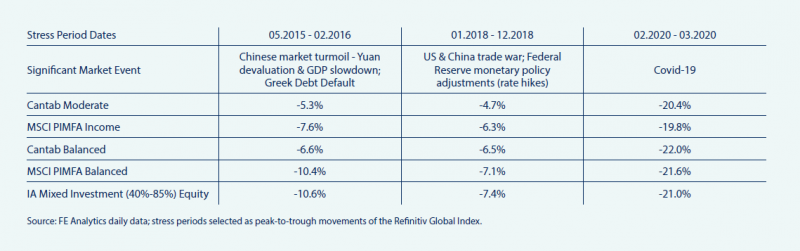

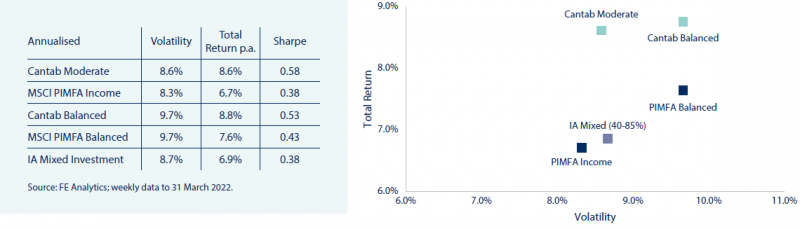

With the exception of the Covid-19 market shock in early 2020, in which performance was relatively in line, Cantab portfolios have been particularly resilient during the market correction of 2018 and the Chinese market induced volatility of 2015. The IA Mixed Investment sector and the PIMFA benchmarks produced inferior risk-adjusted returns when compared to the Cantab portfolios over the last ten years. This is illustrated below:

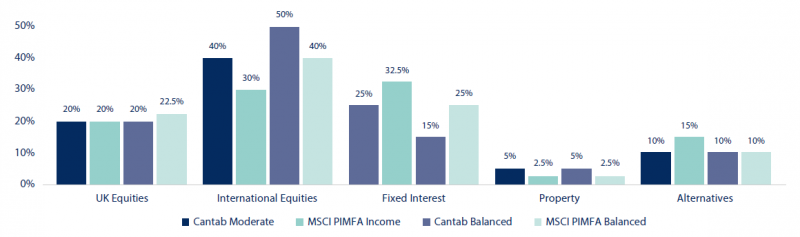

Portfolio Positioning

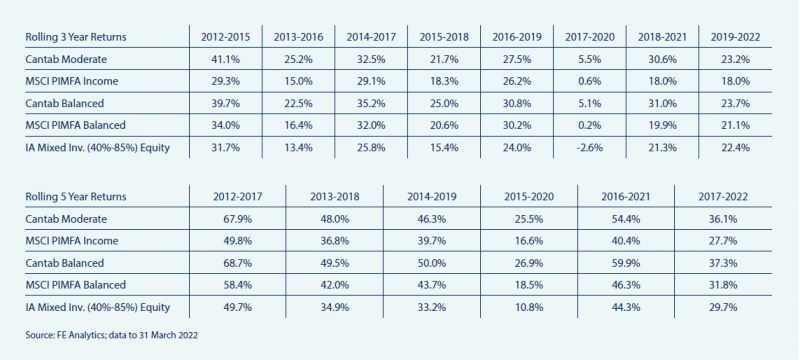

Taking a Long-Term View

Using three and five-year rolling performance periods over the last decade, the Cantab portfolios achieved sizeable outperformance over their respective benchmarks. We, therefore, continue to advise our clients to take a long-term view on investment decisions, looking beyond short-term volatility.

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.