The recent falls in the UK and US inflation rates have been well received by both bond and equity markets. However, as economic and market uncertainty persists, we continue to see challenges ahead for policymakers. Inflation remains sticky, particularly in the UK and Europe, with labour market tightness and associated wage growth presenting renewed pressure on both the demand and supply side. The US is further along in the cycle, with credit growth having slowed significantly and core inflation moving in the right direction. Outside of the Western developed markets, Japan appears well positioned economically, with India, China and other Asian markets facing different drivers from those seen in the West.

Year to date performance of parts of the US market demonstrate how quickly and significantly asset prices can recover as fundamentals evolve. We do not believe that the Big Tech bounce is yet reflective of an imminent wider recovery for equities, but we retain confidence that with time, wealth creating companies will once again drive attractive returns for investors. As rates have risen, bonds are once again providing real yield opportunities. Whilst the short-term outlook for bonds remains clouded, there are clear positives in having options in this space for financial planning purposes.

For Private Clients, there continue to be planning opportunities to employ tax efficient structures to improve net returns.

The lifting of the pension lifetime allowance charge and the increased annual contribution limits may allow those who have stopped contributing to re-commence and those limited by the previous lower limits to increase their annual contributions. Where pension contributions have not been made in recent years, it is potentially possible to take these up for three previous tax years. Where applicable, please request advice from your Client Director to assist.

International life assurance bonds can provide a tax efficient way to save for the future and provide estate planning opportunities to protect against inheritance tax. These bonds can also provide a mechanism to gift money to your family or friends. They provide a means to defer tax by rolling up investment gains without immediate tax charge and provide an additional structure for diversification where not already utilised.

There are opportunities to mitigate inheritance tax through careful financial planning and potentially the use of business relief on certain assets. The possibilities and options for consideration should be discussed with your Client Director, if relevant for you.

This Outlook will touch upon the following topics:

1. Winners and losers in recent market performance

2. Concentration of US equity markets and its implications for investors

1. Recent market performance

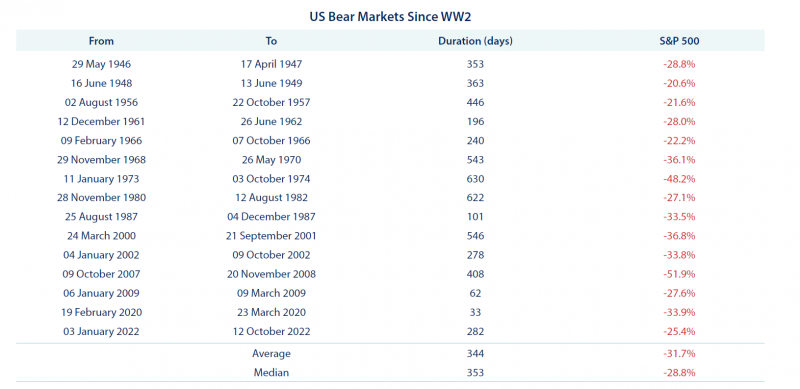

Last year’s market performance took the US index into Bear market territory – the first protracted downturn since 2008. The index lost a quarter of its value – statistically a relative ‘mild’ contraction relative to historic bear markets.

Source: reproduced from Seeking Alpha, “The complete history of bear markets”, 2022, FE Analytics 2023.

Past performance is no guarantee of future results.

But these numbers do not tell the full story for UK-based investors in Global portfolios. The US Dollar appreciated by >20% against Sterling over the same period, a move which has been almost entirely reversed in the nine months since October lows. Where Sterling weakness dampened the downside for US assets in 2022, Sterling strength has muted the recovery.

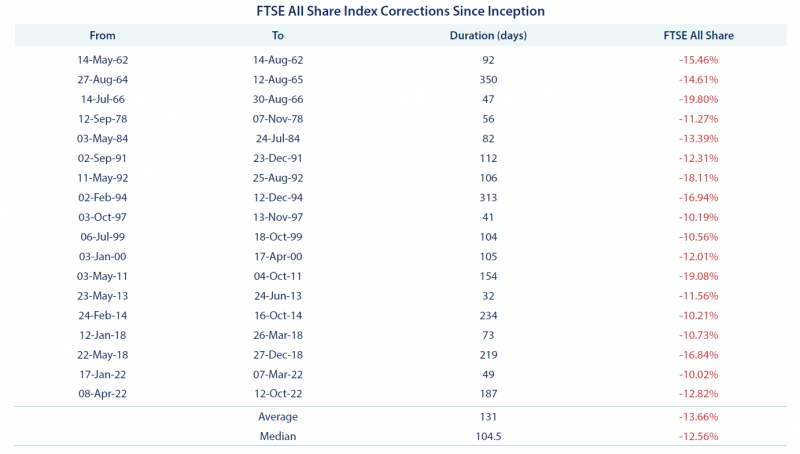

For UK equities, the drawdown in 2022 was firmly in ‘correction’ rather than bear market territory when considered in aggregate. Once again however, the numbers mask underlying variation both in the downwards movement and subsequent ‘recovery’.

Source: Refinitiv. Price return, £. Daily data. Past performance is no guarantee of future results.

Source: Refinitiv. Price return, £. Daily data. Past performance is no guarantee of future results.

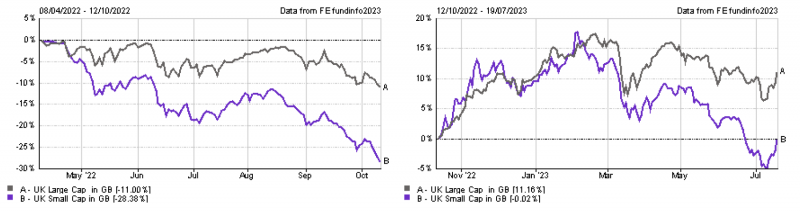

The largest and most internationally diversified stocks in the UK held up much better than the smallest listed companies in 2022. Thus far, their recovery has also been more resilient. This is perhaps unsurprising given the difference in economic sensitivity between larger and smaller companies, as well as the weighting towards Energy and Financials amongst the largest UK names.

The small-mid cap UK market contains a plethora of global leading companies engaging in innovative development. Holdings within our chosen funds include Indivior – a pharmaceutical company specialising in treatment for opioid addiction; Alphawave – a leading designer of advanced silicon technologies with exposure to the growing AI-based silicon chip market; and TI Fluid Systems – a manufacturer of engineered automotive fluid systems for light vehicles, including hybrid and electric vehicles.

The small-mid cap UK market contains a plethora of global leading companies engaging in innovative development. Holdings within our chosen funds include Indivior – a pharmaceutical company specialising in treatment for opioid addiction; Alphawave – a leading designer of advanced silicon technologies with exposure to the growing AI-based silicon chip market; and TI Fluid Systems – a manufacturer of engineered automotive fluid systems for light vehicles, including hybrid and electric vehicles.

Outside of equity markets, bonds, infrastructure and property have all weighed heavily on the performance of diversified portfolios over the last 18 months. There has been little recovery in these areas year-to-date – indeed infrastructure assets have declined by a further >10%. Whilst this is uncomfortable, it is not entirely surprising given the continued upwards pressure on interest rates. Where investors can attain 5% or more in short-dated government backed securities, the demand for yield-producing asset classes such as infrastructure and property has fallen. We note however that many of the underlying assets within these sectors retain strong cashflow profiles, often with inflation linkage. As interest rates approach their likely peak, we believe that demand for high quality assets in structural growth areas, paying reasonable yields, will return strongly.

Looking through the noise generated by macroeconomic and political developments, the overall health of corporates both in the UK and across other markets remains, in our view, robust. Whilst we continue to believe that there will be pockets of difficulty as market participants adjust to a higher rate environment, we remain confident that companies will continue to innovate and grow. We also note that index returns are discussed in nominal terms – i.e. we make no adjustment for inflation when quoting index levels. Companies with pricing power should be able to grow their earnings with (or close to) inflation. As the environment improves, we would expect these higher earnings to be valued accordingly by market participants, making it ever more important to seek out high quality franchises with strong competitive positions.

2. Concentration of US equity markets

As excitement around Artificial Intelligence (‘AI’) has grown this year, so too has excitement around the so-called FANGMAT stocks (Facebook/Meta, Apple, Nvidia, Google/Alphabet, Microsoft, Amazon, Tesla). These seven have risen between 40% and 180% this year, sending their valuation multiples well above their average over the last decade. NVIDIA now has a P/E of >200x and the big 7 have a forward P/E of over 30x – the rest of the S&P 500 is trading at a more conservative 16x. These valuations have ballooned on the back of sentiment as opposed to any change in fundamentals thus far – the average trailing 12-month revenue growth for Meta, Amazon, Netflix, Alphabet, Apple and Microsoft has been trending downwards from 40% to 5% over the last 20 years and is now at its lowest y-o-y revenue growth rate since 2008.

The performance of the S&P 500 index is the most concentrated it has been since the 1970s, adding 14.5% in the first six months of this year whilst the S&P 500 on an equal-weighted basis is up less than 5%. Those seven companies are more than 25% of the entire index and Apple is worth more than the FTSE100.

Whilst we are concerned around the outlook for these names in the event that earnings growth does not bring valuation multiples to a more reasonable level, we do not see a wider market environment consistent with a repeat of the dot-com bubble. The late 1990s saw an IPO mania of internet-based companies jumping on the hype train, which we haven’t seen this time around, IPOs have been few and far between. Additionally, the dot-com era saw share prices skyrocket in profitless tech companies, this time around the big seven are highly profitable, Tesla, for example, commands the largest profit margins of any automaker let alone its EV peers.

One could also argue that the meteoric rise this year is just a recovery from last year’s sell-off; markets were perhaps pricing in a steep decline in earnings in 2023 for which we have seen a big turnaround in analyst forecasts. Whilst earnings are still expected to decline modestly in Q2, they are now expected to rebound strongly in Q4 after a relatively flat Q3. Analysts are also expecting Amazon, Meta and Nvidia to post 100% y-o-y EPS growth in the final quarter.

The level of concentration seen in this year’s US market rally has left most active managers well behind benchmarks. The risks to passive strategies should we see a reversal in fortune for these largest names are significant. We believe that there are opportunities across the US and Global equity space to benefit from advancements that AI will bring – these are not limited to technology names. There are broader reasons to be positive on US equities outside of these names: the US economic picture is looking clearer with the monetary cycle more advanced than other developed markets. The companies making up the S&P 500 are in a healthy aggregate position to withstand possible economic jitters with net debt / EBITDA sitting close to 30-year lows. Policymakers are looking to fiscal stimulus to drive growth towards the tail end of the election cycle. Whilst we are not clear that the names currently driving market performance will be the ones to deliver the gains of the next cycle, we do believe that the US remains a very attractive market for long-term wealth creation.

24 July 2023

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.