The first weeks of 2023 have seen investors optimistic at the prospect of peaking inflation. Most commentators are in agreement that the initial step down towards low-mid single digit levels of inflation is likely to be relatively quick and pain-free from this point forwards. How and when Central Banks are able to restore price stability at the 2% target level is less certain and we continue to believe that many developed markets will tolerate higher levels of inflation in the medium-term, in part as a means to reduce the impact of pandemic-related debt.

The relationship between economic developments and market movements has never been straightforward. Investors driving market movements are inherently forward looking and prone to behavioural biases in a way that fundamental economic data is not. Excessive optimism or pessimism is rarely reflected in macroeconomic data to anywhere near the same degree as it is seen in investment markets.

Simultaneous declines in equity and bond markets are infrequent. For many investors driven by fundamental investment philosophies, 2022 was one of the worst years on record for returns. As one of the world’s largest investors, owning on average 1.3% of every global listed company, Norway’s sovereign wealth fund is a reasonable proxy for ‘passive’ participation in the investable universe. The $1.3tn fund shed $164.4bn in 2022, a decline of 14.1%. This represents one of the worst results in the fund’s history, second only to 2008.

In times of uncertainty, we believe that it is more important than ever to revert to our long-term asset allocation and fund selection principles. Changes made over the last year have left Cantab portfolios balanced and we hope, resilient to future volatility. Alongside considering the portfolio wide impact of changes, we continue to focus on ensuring that individual elements of the portfolio provide the potential for long-term growth. Events of 2022 have changed the investment environment significantly – the opportunity for reasonable ‘risk-free’ yields is more attractive than it has been through the recent cycle.

In this outlook article, we discuss the improved outlook for fixed interest in a new economic paradigm. We also explore the ways in which portfolio construction, tax optimisation and gifting / estate planning can add value for clients during periods of heightened uncertainty.

1. Fixed Income – A New World?

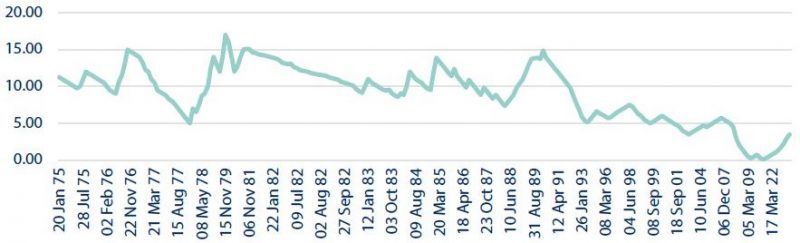

2022 was not kind for bond investors. Where one has come to expect bonds to provide security in the face of equity market drawdowns, 2022 proved to be a year with concurrent falls – a rare occurrence. Why? Central Banks are talking a tough game on tackling inflation and backing it up with rate rises. Although these rises look aggressive from their starting point, in absolute terms interest rates remain low relative to long-term history.

Bank of England Base Rate 1975 – Present

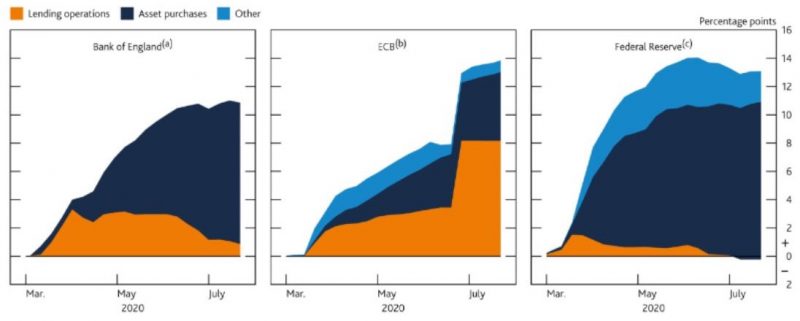

Perhaps just as significantly, interest rate increases come in the context of Central Bank balance sheets which have ballooned to levels never before experienced. In the UK, the Bank of England’s Quantitative Easing programme has left an unprecedented quantity of bonds held centrally. The Federal Reserve and European Central Bank have had similar experiences.

The breakdown in functioning of the UK Gilt market following September 2022’s mini-budget provides an example of the potential challenges associated with a highly concentrated holding base. Whilst the Bank of England was able to restore order relatively quickly, the question arises – what will be the implications of a shrinking in Central Bank balance sheets over the coming years? How will market liquidity be impacted and what will the market look like once Central Banks step back from their role as buyer?

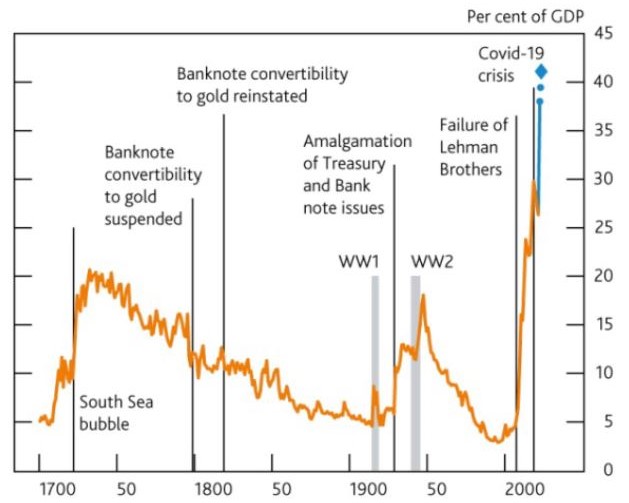

Chart 1: Bank of England balance sheet as a % of GDP

Source: Bank of England ‘The Central Bank Balance Sheet as a policy tool, past, present and future’

Chart 2: Central Bank Balance Sheet response to Covid Crisis

(a) Bank of England lending operations shown here: Indexed long-term repo, Contingent term repo facility, US dollar repo operations, Liquidity Facility in Euros, Term Funding Scheme and Term Funding Scheme with additional incentives for SMEs. Bank of England asset purchases shown here: Asset Purchase Facility and Covid Corporate Financing Facility.

(b) ECB lending operations: Lending to euro-area credit institutions related to monetary policy operations denominated in euro. ECB asset purchases: Securities held for monetary policy purposes.

(c) Federal Reserve lending operations: Repurchase agreements, Loans and Net portfolio holdings of TALF II LLC (less TALF II LLC Treasury contributions and other assets). Federal Reserve asset purchases: Securities held outright.

Source: Bank of England, Bureau of Economic Analysis, European Central Bank, Eurostat, Federal Reserve Board, ONS and Bank calculations. In: Bank of England ‘The Central Bank Balance Sheet as a policy tool, past, present and future’

We anticipate that the road ahead is unlikely to be perfectly smooth for bond markets. However, mid-high single digit yields on government and investment grade debt are hugely attractive relative to what was on offer over the last decade. We have written in previous Outlook articles about our unwillingness to lock in negative multi-decade returns by purchasing bonds at prices providing negative yields. The sub-zero yield phenomenon appears to have vanished, with the market value of negative-yielding bonds in the Bloomberg Global Aggregate index falling from over $18tn in early 2021 to zero today.

We now view bonds as once again providing a viable alternative to equity allocation, in their own right. Currently, investors are not rewarded for taking on significant interest rate risk in the form of longer duration bonds. Nor do we believe that credit risk is being well priced in the context of potential future recession. We therefore favour short to medium duration developed market government and investment grade debt and this is reflected in our fixed income allocations within portfolios.

2. Opportunities for Financial Planning in Uncertain times

As markets present challenges, the importance of financial planning is drawn increasingly into focus. We explore below the impact portfolio construction can have in addressing sequencing risk; the importance of tax optimisation; and factors to consider in gifting and estate planning.

Portfolio Construction

A common problem in retirement is sequencing risk – extracting cash from a portfolio which may lose value resulting in more investments being sold. The depletion may be exacerbated by high inflation as portfolio withdrawals are increased to keep pace with increasing expenditures.

A well-designed multi-asset portfolio should mitigate the level of volatility and maximum drawdown of investments. Moreover, the careful selection of investments with low and negative correlation to one another can enable an investor, when they require income during market downturns, to not be forced into raising cash from assets at a low point. As such, this should reduce sequencing risk and improve portfolio longevity.

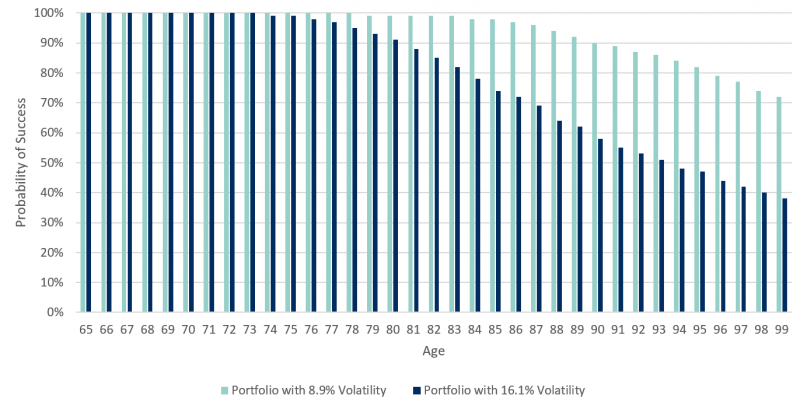

The graph below highlights the impact of volatility on the probability of success of withdrawing £40k per annum (increasing with inflation) from a £1m portfolio as age increases.1 Both portfolios have the same average expected return (5.9%), however, the level of volatility differs – representing a balanced portfolio compared to one that carries greater risk. For reference, Cantab’s Moderate portfolio (Risk 5) over the last 10 years has returned 7.3% per annum with an average volatility of 8.9%, whilst the FTSE 100 has endured 15.3% volatility (with a 6.3% annualised return).2 As is evident, a well-diversified portfolio with lower volatility increases the chances of a successful financial retirement.

Tax Optimisation

The Autumn Statement on 17 November 2022 increasing personal taxes, has focused the mind on tax optimisation and naturally leads to a sense check of existing arrangements.

In our view, diversification should be present within a client’s investment structures as well as the investments. In an economy where tax legislation is constantly changing and evolving, it is prudent to have multiple capital and income options available through exposure to a variety of tax wrappers. There is much to be gained, both in tax savings and increased adaptability, by utilising allowances available to an investor and family via different accounts (General Investment Accounts, ISAs, Pensions, Offshore Bonds, VCTs etc.). The Autumn Statement, amid an array of measures to tighten fiscal policy, has curtailed the dividend and capital gains tax allowances. For clients, this may increase the attraction of investing internationally; however, specialist advice is recommended on this point as products can be complex and their suitability will vary for each client.

The table below demonstrates the significant tax savings possible by withdrawing across various tax wrappers and utilising one’s allowances, assuming there is 50% growth on the investments.

| £2m General Investment Account | £1m Pension | £3m Offshore Bond (£2m Initial Premium) | £500k ISA | |

|---|---|---|---|---|

| Tax due if £200k is withdrawn from only one account | £7,103.33 | £52,460 | £25,232 | £0 |

| Tax due if £50k is withdrawn from each account (£200k in total) | £436.66 | £4,986 | £0 | £0 |

Table Notes: £12,300 CGT allowance (2022/23 tax year) – if the allowance was £3,000 (2024/25 tax year), the figures would be £8,963.33 and £1,366.66 respectively. The pension income in this table is taken as a UFPLS (25% tax-free) – it is worth noting that extracting money from a pension brings those assets back into one’s estate for inheritance tax purposes. Offshore bond income is utilising the 5% tax-deferred annual withdrawals, assuming the allowance has been utilised in all prior policy years and no top slicing relief is available – any excess has been treated as a chargeable gain and the Personal Allowance, £5k Starting Rate for Savings and Personal Savings Allowance have been utilised. ISA investment gains, income and withdrawals are tax-free. No other income (e.g. state pension, natural income from the general investment account, rental income from properties etc.) has been included.

Gifting and Estate Planning

‘How much can I afford to give away?’ is a question to which the answer has become more uncertain in the current economic climate. The desire to gift in order to financially support others or to reduce the size of one’s estate potentially liable to inheritance tax is a common financial objective for clients. However, in an inflationary environment, it becomes harder to predict one’s capacity to gift assets as the monetary amount of income required in the future rises significantly.

Cantab supports clients by providing cash flow analysis to determine capacity to gift. Once established, outright gifting in most cases would be the best option, whether that be a direct gift or a gift into trust. Understandably, there is often concern with this approach due to the uncertainty of future requirements, however, there are solutions for those who are unable to or are nervous about gifting outright.

Methods which enable people to gift more flexibly can be attractive, particularly in such periods of uncertainty. These can enable clients to make gifts whilst retaining an element of access to the capital if required. For example, flexible reversionary trusts and loan trusts can be used by those looking to mitigate a potential inheritance tax liability but are uncertain about their capacity to make outright gifts. Once again, expert advice is recommended due to the complexity of these solutions and the varying suitability for each individual or family.

Conclusion

Markets often experience wild swings from optimism to pessimism and back again. It can be hard to keep track of the interaction between fundamental drivers and sentiment-related movements. We continue to consider this time as a period of unusually high uncertainty, although economically the environment is far from exceptional in the context of history.

In this environment, focussing on portfolio construction goals and financial planning priorities is likely to yield the best long-term results. Our investment team continues to assess the likely impact of ongoing developments and evolve portfolios accordingly. We remain cautiously optimistic that there are opportunities arising which should present attractive outcomes for clients going forward.

1 Monte Carlo simulation run on Voyant with 1,000 iterations at an assumed annual growth rate of 5.9% and 2.5% annual inflation. Taxation of income and growth of investments has not been factored in.

2 Source: FE Analytics, data as at 10/01/2023.

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.