Global ESG assets under management are to exceed $53 trillion by 2025, according to Bloomberg Intelligence, reflecting the increased investor appetite for sustainable investment solutions. The growth is especially evident in Europe, which accounts for half of global ESG assets, but the US experienced the strongest expansion in 2021 and might possibly dominate the space in the future1. Passive ESG strategies in the US have also gained momentum in recent years outpacing net inflows of actively managed counterparts2. This paper takes a deeper look at the relationship between passive strategies and ESG investing, whilst considering the challenges and pitfalls associated with following a passive approach to ESG integration. Interesting findings include:

- Goal alignment requires active due diligence to avoid ‘greenwashing’.

- ESG rankings are inconsistent across providers and, therefore, provide an uncertain foundation for ESG portfolio construction, particularly when using quantitative methods.

- ESG and passive investing may, in fact, be mutually exclusive.

How ESG is the entire market?

Active ESG investment processes typically follow rigorous screening procedures to ensure that the underlying holdings of a solution are aligned with the sustainable objectives outlined in the investment mandate. As one would expect, investing in the entire market does not lend itself to these processes and thereby removes investor choice with respect to personal ESG preferences. The table below outlines the fossil fuel and deforestation exposure of a popular non-ESG tracker fund for comparison with the ESG tracker funds in the section to follow:

Analysing fossil fuel exposure in the Vanguard S&P 500 ETF shows that approximately $58bn of the $855bn assets are invested in fossil fuel securities – a total of 51 equity holdings representing overall fossil fuel exposure of 6.8%3. Surprisingly, Refinitiv presents the ETF with a relatively high ESG rank of 70, despite it not emphasising ESG or Sustainable investing. This reinforces the importance of transparency for professional investors when advising clients and making them aware of possible pitfalls.

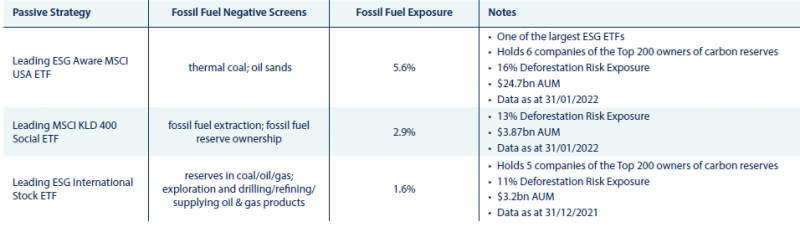

How ESG are ‘passive’ ESG solutions?

In the fourth quarter of 2021, Morningstar reduced the number of funds in Europe that it now recognises as sustainable by 27% due to the additional classification requirements of the EU Sustainable Finance Disclosure Regulation (SFDR)5. Not only does this highlight the scale of greenwashing that existed but also the challenges associated with identifying legitimately sustainable products. These challenges are just as prevalent in the ‘passive’ ESG space, which we illustrate in the table below:

Each of the strategies above is ESG labelled and ESG-themed in its screening approach, which simplifies the process for passive and fee cautious investors to invest alongside ESG principles. However, this represents one pitfall of ‘passive’ ESG solutions – it is perceived to screen out controversial sectors but likely only screens out subsectors of controversial sectors. This leaves investors with material exposure to the types of companies they would typically (and likely thought they did) avoid. Relatedly, research produced by Planet Tracker6 proposes that ETFs disseminate the risk of deforestation in equity and bond markets. This represents potential ‘hidden’ risks of which investors remain unaware. For example, the ESG Aware MSCI USA ETF has the same deforestation risk exposure as the non-ESG themed Vanguard S&P 500 ETF outlined earlier, illustrating the difficulty in aligning the ESG preferences of clients with a passive solution.

Hard Sector Exclusions

Hard sector exclusions are amongst the most sensible ways to avoid the pitfalls outlined previously. However, this might significantly increase the tracking error of a fund to the extent that it can no longer be labelled as ‘passive’. Passive strategies typically have a tracking error ranging between 1% and 2% whereas active strategies typically range between 4% and 7%7. For example, the actively managed VT Cantab Sustainable Global Equity Fund screens out the entire energy sector to avoid fossil fuel exposure. It also screens out armaments, gambling, alcohol and tobacco, and has a tracking error of 7.8%8. This reinforces the notion that hard exclusions are an active requirement when aligning investments processes and individual preferences with ESG.

ESG Ambiguity and Goal Alignment

Since the introduction of the Paris Agreement during the COP21 summit in 2015, the formalisation of ESG-aligned investing principles has significantly accelerated. However, what constitutes ESG remains uncertain, which has led to a substantial number of funds in Europe no longer being recognised as sustainable. Placing this in the context of active vs passive ESG investing, the latter is, at its core, a mandatory deviation from the market as the entire market does incorporate securities that do not comply with what is becoming the industry standard. In other words, investing passively in an ESG-aligned solution does not only complicate the process of aligning the specific ESG goals of an investor with an investment solution but completely removes active ESG due diligence that goal alignment requires.

ESG Rankings

ESG rankings are increasingly being used in the development of sustainable products and academic research has shown that ESG rankings do correlate with long-term performance. However, the challenge for the active manager is deciding between ESG ranking providers who tend to score companies differently. Research by Research Affiliates found that the methodologies adopted by ESG ranking providers are not consistent and can lead to drastically different outcomes in portfolio construction9. Tailoring a product based on the ESG preferences of clients requires a more sophisticated approach alongside further ESG due diligence. This level of ESG due diligence is a requirement in concentrated actively managed ESG mandates but is unlikely to be thoroughly adopted in passive strategies that hold a substantial number of holdings.

Summary

Aligning the ESG preferences of clients with a passive investment approach is far from simple, especially given the rate at which the ESG investment landscape is evolving in terms of measurement standards. Most importantly, client preferences lay the foundation for goal alignment and are unlikely to be achieved without active intervention. An environmentally poor, socially irresponsible, and inadequately governed company is unlikely to present a compelling investment case. It is therefore difficult to justify investing in a strategy that does not actively conduct thorough ESG due diligence.

1 Bloomberg Intelligence, ESG assets may hit $53 trillion by 2025, a third of global AUM (2021); 2 Morningstar, Sustainable Funds U.S. Landscape Report: Record Flows and Strong Fund Performance in 2019. (2020); 3 Other controversial sector exposures such as Armaments, Tobacco, Gambling, Alcohol, Pornography and Contraceptives were not included in this analysis and goes beyond the scope of this study; 4 Fossil Fuel Exposure obtained from Fossil Fuel Funds, Available: https://fossilfreefunds.org/; Deforestation Risk Exposure obtained from Deforestation Free Funds, Available: https://deforestationfreefunds.org/; 5 Wealth Manager, Morningstar culls $1.2tn worth of European sustainable funds, (10/02/2022); 6 Planet Tracker, Exchange-Traded Deforestation (2020); 7 Informa, Tracking Error, Available: https://financialintelligence.informa.com/; 8 Source: FE Analytics 1 year to 31 January 2022; 9 Research Affiliates, What Difference an ESG Ratings Provider Makes! (2020)

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.