Introduction

In March 2021, the European Union’s Sustainable Finance Disclosure Regulation (EU SFDR) formally came into effect, with the objective of standardising sustainability disclosures to assist asset owners and retail clients in understanding, monitoring, and comparing the sustainability characteristics of investment products. In July 2021 the UK Chancellor, Rishi Sunak, announced the Sustainability Disclosure Requirements (SDR)1, which are closely aligned with the aims and objectives of the EU SFDR2. These requirements are expected to be formalised in 2022. The Financial Conduct Authority’s (FCA) November 2021 Discussion Paper3 outlines the expected disclosures, which are summarised in this note.

Investment Product Disclosure

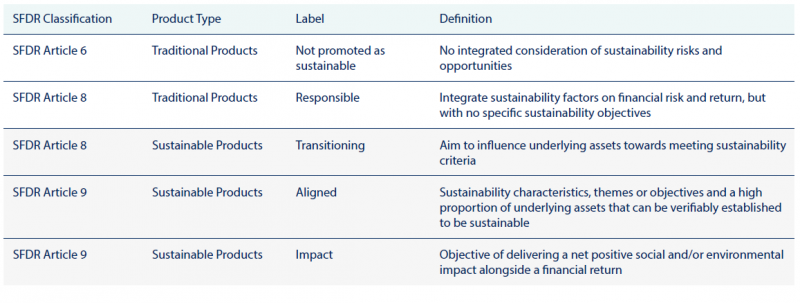

A new sustainable investment labelling regime will be established under the SDR, reflecting products’ sustainability impact and the relevant financial risks and opportunities. The details of the regime have not been released, however, the FCA has produced a potential framework for sustainability labelling of investment products. Products must meet the criteria for ‘transitioning’, ‘aligned’ or ‘impact’ products in order to be labelled as ‘sustainable’, whereas products with more modest ESG ambitions may be labelled as ‘responsible’. The SDR may not use the ‘Article’ style labelling of the EU SFDR, but an indicative mapping to the EU SFDR’s Article labelling system is summarised below:

Asset Manager and Asset Owner Disclosure

Asset managers and asset owners will be expected to disclose how they incorporate sustainability in their governance arrangements, investment policies and strategies. It is not yet clearly defined as to what the exact disclosure requirements will be, however, the FCA states that they are likely to build on the Task Force on Climate-Related Financial Disclosures (TCFD). The scope of these disclosures will be expanded to encompass a broader set of ESG factors, rather than solely focusing on climate change. This plan aims to support prospective clients and consumers choosing between new managers, determine whether the management of their assets matches their sustainability preferences, and hold their managers to account if they are lagging with respect to sustainable investing.

Corporate Disclosure

Under the SDR, corporations are required to follow the standards set by the International Sustainability Standards Board (ISSB)4 and report their environmental impact using the UK Green Taxonomy. Firms will also be required to disclose their transition roadmap and how it is aligned with the government’s net-zero carbon emissions commitment or explain why they have not done so. These requirements will encourage consistency and enable comparability in published plans of UK corporates. With companies becoming more transparent about their carbon footprint and the actions taken in this regard, the SDR aims to support investors wishing to follow a sustainable approach to their investments.

Impact on Financial Advisors and their Clients

The myriad of existing regulations still applies and, as such, the SDR can be viewed as an extension to present disclosures and practices required by financial market participants and financial advisers. In principle, the SDR is designed to create greater clarity around investment products and eliminate the confusion surrounding sustainable investing. Financial advisers can use the labelling regime to guide investments and inform clients about the investable products available to them and the ESG mandate of such products. All the while, advisers will need to ‘walk the walk’, ensuring that their own business is incorporating sustainability into its strategy and processes. The disclosure requirements discussed in this note will largely be written throughout 2022, with certain extensions, subject to consultation, being formalised over the next two to three years.

1 HM Government (October 2021), “Greening Finance: A Roadmap to Sustainable Investing”

2 Official Journal of the European Union (November 2019), “Regulation (EU) 2019/2088 of the European Parliament and of the Council of 27 November 2019 on sustainability-related disclosures in the financial services sector”

3 Financial Conduct Authority (November 2021), “Sustainability Disclosure Requirements (SDR) and investment labels”

4 The International Financial Reporting Standards (IFRS) Foundation is the international body that governs the setting of global accounting standards. It recently established an International Sustainability Standards Board (ISSB) to develop global baseline reporting standards for sustainability, building on the work of the TCFD.

Risk warnings

This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future. It is important to note that in selecting ESG investments, a screening out process has taken place which eliminates many investments potentially providing good financial returns. By reducing the universe of possible investments, the investment performance of ESG portfolios might be less than that potentially produced by selecting from the larger unscreened universe.