1 February 2023

Fund Overview

What is the name of the fund?

The VT Cantab Sustainable Global Equity Fund.

What is the fund’s investment objective?

The fund seeks to generate superior risk-adjusted equity returns with a robust and disciplined investment process that focuses on investing in quality companies at attractive valuations and holding them for the long term, whilst integrating Environmental, Social and Governance (ESG) factors into the construction of the portfolio.

What ESG restrictions are in place?

The fund will not invest in companies involved in the production or extraction of fossil fuels or those engaged in the alcohol, tobacco, gambling and/or armaments industries. In addition, quantitative and qualitative analysis is used to assess whether companies pay due attention and consideration to ESG concerns and demonstrate this through ESG policies and practice.

What is the investment opportunity?

While many asset owners remain focused purely on the generation of financial returns, the growth of ESG investing is undeniable and undeniably appropriate, in our opinion. Indeed, the world is warming up to the belief that we need to invest more responsibly, certainly in terms of how we treat the environment, but also with respect to how corporations behave from a social and governance perspective.

How many stocks will the fund own?

The portfolio is relatively concentrated (c30-35 stocks on average) but is well diversified both by region and industry.

Do COP26 and 27 commitments affect investment decisions?

As we progress through the current decade and beyond, it is clear that the commitments pledged at COP26 and COP27 are likely to create a tailwind for various sectors and industries whilst creating a headwind for others. Most notably, the data and analytics industry are likely to benefit from greater and more sophisticated demand in emissions reporting, particularly in the wake of the implementation of the UK Sustainability Disclosure Requirements (SDR). One of the main outcomes of COP26 was a pledge to end deforestation by 2030. As a result, companies that contribute to deforestation are likely to feel more pressure going forward. More broadly, the acceleration in Green Finance is likely to serve the renewable energy and infrastructure sectors. For example, Joe Biden’s Inflation Reduction Act committed $369bn in subsidies and tax breaks for green infrastructure businesses and those supporting the transition to renewable energy. Furthermore, the emphasis placed on zero-emissions transport will likely see increased sales of electric vehicles (EVs), boosting demand for EV component parts and EV infrastructure too. These developments are likely to have various investment implications in the form of asset allocation, portfolio construction and long-term risk management but also create opportunities for investing in companies that support, and will therefore benefit from, the transition.

What investment style will the manager adopt?

The portfolio is well balanced between Quality and Value styles, Responsible and Sustainable investments, and also balanced by vintage – given the low turnover of stocks owned, the portfolio will at any point in time have a mixture of recently purchased companies and companies that have been held for many years.

We believe this combination of conviction, high active share, and patience will reward investors over the long term. Indeed, studies of equity fund performance have shown that such strategies have the best chance of outperforming. Please see further detail in the Investment Philosophy and Process section.

What is ESG?

It is easy to feel confused about ESG investing today. The media – and investment industry – are awash with differing interpretations of what is often being portrayed as a relatively new style of investing.

We see it differently. To us, ESG is merely a modern interpretation of an age-old concept that companies are not run purely for the benefit of their shareholders – there are other stakeholders to be considered.

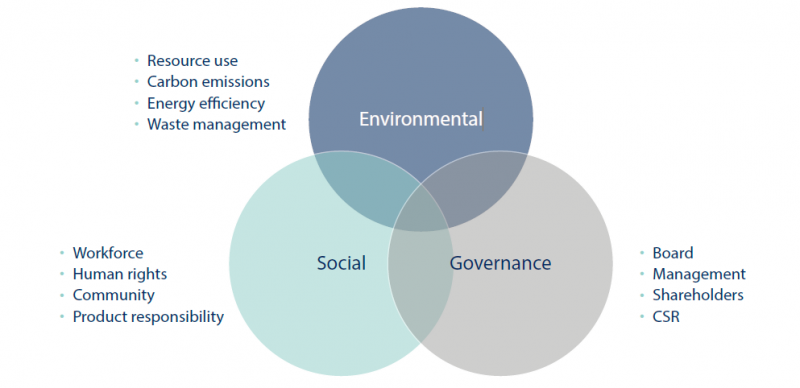

Specifically, corporations are becoming increasingly aware of their Environmental responsibilities in terms of, for example, carbon emissions and waste management – future generations are the obvious stakeholders in this regard.

In addition, companies are coming under increasing pressure to show Social awareness in their treatment of their own workforce and the wider community. Finally, good Governance aligns the interests of boards and management teams with shareholders and other stakeholders.

How does ESG fit into the Investment Process?

It is important to recognise that, while the media may focus on one specific aspect of these ESG building blocks at any point in time, as investors we need to maintain a balanced approach to all the stakeholder issues a company might face.

From an investment perspective, while the above considerations are embedded into our investment process, our overriding aim is to generate superior investment returns for our clients.

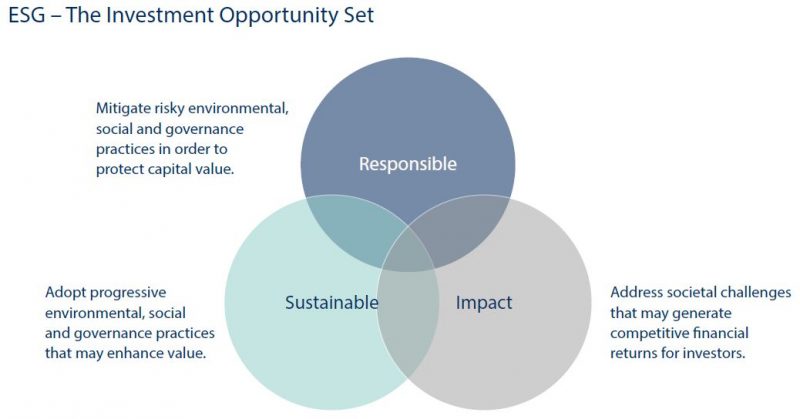

In this context, we see the investment opportunity set as a spectrum ranging from Responsible investing, which seeks to protect capital by avoiding poor ESG practices, through Sustainable investing, which adopts progressive practices that may enhance value, to Impact investing, which addresses ESG challenges that may or may not generate financial returns.

On a risk-adjusted basis, therefore, we believe Impact investing alone may inhibit the ability to satisfy our financial goals. As such, we expect the fund’s portfolio will be balanced across these three opportunity sets.

What ESG data do you use?

For quantitative ESG analysis, we use Refinitiv as our third-party data provider. Refinitiv is a leading global data provider, and offers one of the most comprehensive ESG databases in the industry, with over 150 content research analysts trained to collect ESG data covering over 7,000 public companies globally.

Sourcing from annual reports, company websites, NGO websites, stock exchange filings, CSR reports and news sources, a subset of the most comparable and relevant data fields is used to power the overall company assessment and scoring process.

A company’s ESG performance is measured across ten main themes, grouped under Environmental (resource use, emissions, innovation), Social (workforce, human rights, community, product responsibility) and Governance (management, shareholders, CSR strategy). There is significant overlap between these themes and the ten principles of the UN Global Compact, which cover Human Rights, Labour, the Environment, and Anti-Corruption.

What are the limitations of ESG data?

There can be a wide discrepancy between different data providers’ scoring systems; and there is the possibility that companies may be able to ‘greenwash’ their credentials.

How do you mitigate the challenges associated with using quantitative ESG data?

It is essential for us to look under the bonnet of a company, analysing whether satisfactory processes are in place, and whether there is any evidence that the company is or is not following through on these.

Take Apple as an example. One of its aims is ‘to make products without taking from the Earth’. While this is laudable, is there any evidence that the company is genuinely acting on this aim? As it turns out, there is an abundance of evidence: 100% of Apple’s global facilities are powered by 100% renewable electricity; there has been a 70% decrease in average product energy use in the past 10 years; there has been a 35% reduction in its overall carbon footprint compared to 2015; MacBook Air and Mac mini enclosures are now made with 100% recycled aluminium. Apple may not be an Impact stock, but we are satisfied that it is a leader in its approach to responsible and sustainable growth.

Qualitative ESG analysis is time consuming but worth it – it is no longer good enough for companies to perform on the pitch, we also expect them to behave off it.

Investment Philosophy and Process

What is Cantab’s Investment Philosophy?

Our philosophy is heavily influenced by the concepts of ‘quality at a reasonable price’ and ‘margin of safety’. We believe quality companies can generate superior risk-adjusted returns to investors if they are purchased at an attractive valuation and held for the long term. Above all else, successful investing requires time, discipline and patience.

There will always be a trade-off between the perceived quality of a company and its current valuation. The belief that a good company will always make a good investment is a dangerous one. There is always the risk that the company’s operating metrics and reputation deteriorate, or that an investor’s entry point valuation is too high to generate an acceptable return. Share prices are not always driven by what happens next, but by what happens next relative to what is expected to happen.

For investors with exceptionally long-term investing horizons, this trade-off is possibly less relevant, although one still needs to pick stocks whose quality endures, and even then, run the risk of opportunity cost.

Proprietary CAMBRIDGE equity framework

Developed by Cantab Asset Management, the ‘CAMBRIDGE’ framework is a proprietary technique used to monitor stocks and succinctly summarise the investment case for underlying holdings. The technique involves scoring companies against a range of factors chosen to encompass Cantab’s ESG, quantitative and qualitative analysis. These scores are monitored and updated on an ongoing basis.

What is the fund’s investment process?

The fund’s primary focus is to invest in large, well-capitalised companies. Once we have analysed a company from an ESG perspective, we quantitatively assess the quality of the company in terms of its profitability, growth, leverage and earnings quality.

In terms of valuation, we look for a margin of safety through stocks that appear attractively valued on an historic, relative basis, vis-à-vis themselves and their peers.

Following an initial ESG and quantitative screening, we move to qualitative analysis. We are looking to create an historic profile of the company to better understand its operations and how the business and its financial performance has evolved over time; we assess the sustainability of the company’s quality and earnings power (i.e.: its long-term growth prospects); and we analyse the company’s cash flow dynamics. Importantly, we examine how we could be wrong in our investment thesis.

Finally, while we are not momentum investors, we do prefer to swim with the tide rather than against it. We therefore utilise improving earnings expectations and share price performance in order to help the timing of our buy and sell decisions.

What is the portfolio turnover and what limits are in place on position sizing?

We intend to hold positions for the long term, and so portfolio turnover will be low.

A typical investment size for a new holding will be 3% of the fund, and for risk management purposes we will not let a position grow beyond 6%. In addition, while the strategy is bottom up, we will limit any regional or sector overweights/underweights to +20/-20 percentage points relative to the benchmark.

What are the investment implications of the UK Green Taxonomy?

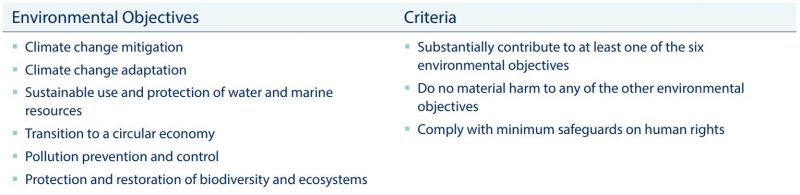

The UK Green Taxonomy is a science-based classification system aimed at accelerating green finance initiatives, by addressing the problem of Greenwashing and thereby supporting the UK’s transition to a net-zero economy. The foundation of the Taxonomy is based on the EU Taxonomy, which outlines that for an activity to be ‘Sustainable’ or ‘Taxonomy-aligned’ it needs to follow at least one of six environmental objectives and meet three criteria, as follows:

The taxonomy will build on existing international taxonomies and will serve as a common framework to set the standard for investments defined as environmentally sustainable in the UK.

Potential investment implications resulting from the Taxonomy implementation are listed below:

- Greater disclosure and transparency requirements are likely to lend structural support to data providers and financial technology companies

- Companies producing enabling products or technologies are also likely benefactors

- Green Finance initiatives might become mainstream sooner and prove attractive for inclusion in investment portfolios

- The integration of governance and social aspects in the estimation of a company’s cost of capital and risk and return profile is likely to reformulate the perception of certain sectors and industry valuations

Liquidity, Transparency and Trust

When can the fund be traded?

Daily liquidity and fund pricing allow investors ease of access and accurate valuations. The fund structure is regulated by the Financial Conduct Authority.

Investment team includes:

Who manages the fund?

The fund is managed by a team led by Mark Wynne-Jones, Leah Bramwell and David Saunderson.

Basic fund details

Name: VT Cantab Sustainable Global Equity A Acc

SEDOL: BK5XL00

ISIN: GB00BK5XL008

Structure: UK UCITS V OEIC

Dealing: Daily/12 noon

Investment Manager: Cantab Asset Management

Authorised Corporate Director: Valu-Trac Administration Services

Depositary: National Westminster Bank

Custodian: Royal Bank of Canada

Risk Warnings. This document has been prepared based on our understanding of current UK law and HM Revenue and Customs practice as at 1 February 2023, both of which may be the subject of change in the future. The opinions expressed herein are those of Cantab Asset Management Ltd and should not be construed as investment advice. Cantab Asset Management Ltd is authorised and regulated by the Financial Conduct Authority. As with all equity-based and bond-based investments, the value and the income therefrom can fall as well as rise and you may not get back all the money that you invested. The value of overseas securities will be influenced by the exchange rate used to convert these to sterling. Investments in stocks and shares should therefore be viewed as a medium to long-term investment. Past performance is not a guide to the future.